Learn the 10-step home buying process for first-time buyers in the US. Understand timelines, key players, and what to expect at every stage.

NMLS#: 1518655

Buying your first home in the US can feel confusing when every step sounds new and high-stakes.

If you’re not sure where to start or how long it takes, you’re not alone. Most first-time buyers go through the same questions. This guide breaks the process into 10 clear steps, so you know what happens, who is involved, and how to move forward with confidence. Understanding the home buying process helps first-time buyers avoid surprises.

Timeline at a glance (10 steps)

- Budget planning: 1 to 2 days

- Pre-approval: 1 to 3 days

- Find a real estate agent: 1 to 3 days

- House hunting: 1 to 8 weeks

- Make an offer: 1 to 3 days

- Under contract: 1 to 2 days

- Open escrow, title, and earnest money: 1 to 3 days

- Home inspection: 3 to 7 days

- Appraisal (ordered by lender): 3 to 7 days

- Underwriting to clear to close and closing: 2 to 3 weeks

Estimated total timeline: 3 to 6 months Contract to closing: 30 to 45 days (according to NAR)

Home Buying Process: The 10 Steps to Buy a Home

1. Budget planning

Who: You, lender

Time: 1 to 2 days

You start by reviewing your income, debt, and savings. A lender estimates your monthly payment using PITI, which includes principal, interest, taxes, and insurance.

Tip: Focus on monthly affordability, not just the home price.

2. Get pre-approved

Who: You, lender

Time: 1 to 3 days

The lender reviews your credit, income, and debt to issue a pre-approval letter. This shows sellers you are serious and ready. If you’re not familiar with mortgage basics, understanding how mortgages work can make the pre-approval process much easier.

Tip: Avoid big purchases during this stage to keep your profile stable.

3. Find a real estate agent

Who: You, real estate agent

Time: 1 to 3 days

Your agent helps you find homes, schedule tours, and guide negotiations. They also explain local market conditions.

Tip: Choose someone responsive and experienced with first-time buyers.

4. Start house hunting

Who: You, agent

Time: 1 to 8 weeks

You visit homes that match your needs, budget, and location. You compare options before making a decision.

Tip: Prioritize must-haves over nice-to-haves to avoid decision fatigue.

5. Make an offer

Who: You, agent, seller

Time: 1 to 3 days

You submit an offer that includes price and contingencies, such as inspection and financing.

Tip: A strong but realistic offer can improve your chances in a competitive market.

6. Under contract

Who: You, seller, agent

Time: 1 to 2 days

Once the seller accepts your offer, both sides agree on terms. The deal moves forward but is not final yet.

Tip: Read your contract carefully so you understand all deadlines.

7. Open escrow and title

Who: You, escrow company, title company

Time: 1 to 3 days

A third party holds funds and documents. You deposit earnest money, usually 1% to 3% of the home price. A title search checks for ownership issues.

Tip: Earnest money can later be applied toward your down payment.

8. Home inspection

Who: You, home inspector

Time: 3 to 7 days

You hire an inspector to evaluate the home’s condition. This helps you uncover issues before closing.

Tip: Use inspection results to renegotiate or request repairs if needed.

9. Appraisal

Who: Lender, appraiser

Time: 3 to 7 days

The lender orders an appraisal to confirm the home’s value. This protects both you and the lender.

Tip: A low appraisal does not end the deal, but you may need to renegotiate.

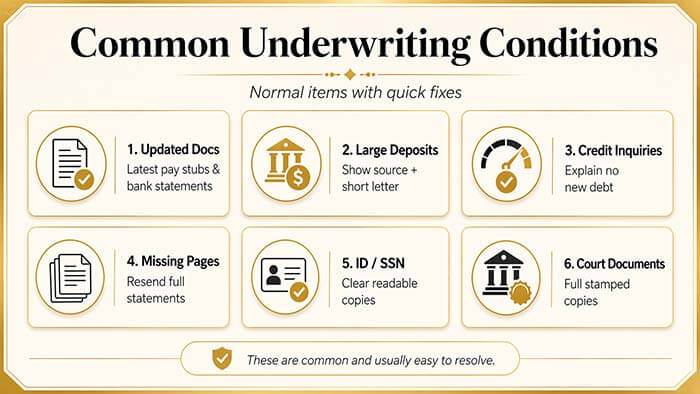

10. Underwriting to closing

Who: Lender, underwriter, you, seller

Time: 2 to 3 weeks

The lender reviews all documents. If approved, you receive clear to close. At closing, you sign the loan documents, and the seller signs the deed.

Tip: Do not change jobs or open new credit before closing.

Common mistakes to avoid

Understanding the home buying process can help you avoid costly mistakes. Many first-time buyers confuse pre-qualification with pre-approval, which can weaken their offer. Others underestimate total costs, including taxes, insurance, and closing fees. Some skip inspection contingencies to win deals, which can lead to costly repairs later. Another common issue is misunderstanding roles. The buyer does not sign the deed at closing, and appraisal is ordered by the lender, not the buyer. Knowing these details helps you avoid delays and surprises.

How to take action

The home buying process becomes much easier when you follow a clear checklist. Start by talking to a lender early to understand your budget and loan options. Then, work with a real estate agent who knows your local market. Build a clear checklist for each step and track deadlines carefully.

Most importantly, take your time to understand each stage. Buying a home is a major decision, and being informed helps you avoid stress and make better choices.

Bottom line

While the home buying process may seem complex at first, knowing each step helps you move forward confidently.

Want to see what you can afford? Talk to a licensed loan officer to explore your options.

Home Buying Process FAQs

How long does the home buying process take?

The process typically takes 3 to 6 months, depending on your financial readiness and local market conditions.

What is the first step in the home buying process?

Most buyers start by reviewing their budget and obtaining a mortgage pre-approval.

Do I need a real estate agent to buy a home?

While not required, an experienced agent can help navigate negotiations, contracts, and local market conditions.

DISCLAIMER:

Wonder Rates NMLS# 1518655. Equal Housing Lender. Information is for educational purposes only and is not a commitment to lend.