Your rate lock is a clock, not a guarantee

Many homebuyers think the hardest part of getting a mortgage is finding a home and locking a rate. Once the rate is locked, it feels like one major uncertainty has been removed from the process.

In reality, a rate lock is not a permanent guarantee. It comes with an expiration date.

The goal is not to assume every transaction will be delayed. The goal is to understand the trade-offs before choosing a lock term.

NMLS #1518655

What a rate lock actually does

A rate lock helps protect you from rising interest rates for a set period of time, typically 30, 45, or 60 days.

If your loan closes before the lock expires, you can generally keep the rate you locked, provided your loan application doesn’t change significantly and you continue to meet the lender’s requirements.

But if your closing is delayed and the lock expires, you may face one of two outcomes:

- You pay a fee to extend your rate lock; or

- Your loan is re-priced using current market rates.

Which outcome applies depends on your lender’s policies, market conditions, and the reason for the delay.

Why closings get delayed more often than buyers expect

Many delays happen for reasons that have little to do with the borrower.

Appraisal delays

Appraisal scheduling can become difficult during busy market periods. If the appraisal report arrives later than expected, underwriting timelines may shift.

Title issues

Title companies occasionally uncover unresolved liens, ownership questions, or documentation problems that must be addressed before closing.

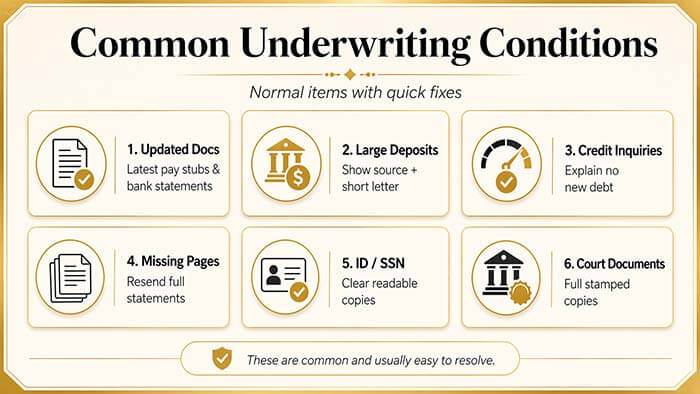

Underwriting conditions

An underwriter may request additional documentation, updated bank statements, employment verification, or explanations for financial transactions.

Each request can add days to the timeline.

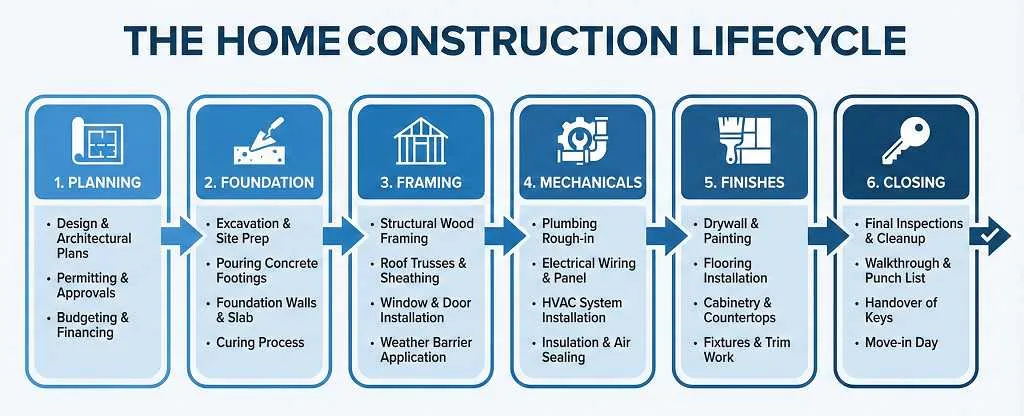

New construction timelines

New construction transactions frequently experience scheduling changes.

Weather delays, labor shortages, permit approvals, utility connections, and final inspections can all push the closing date beyond the original estimate.

This is one reason many buyers of newly built homes evaluate longer lock periods from the start.

Who pays for a lock extension?

The answer depends on the circumstances.

There is no universal rule that applies to every lender or every transaction.

A useful framework is to identify the source of the delay.

Scenario 1: Borrower-caused delay

Examples include:

- Late documentation

- Changes to employment information

- Delayed responses to underwriting requests

- Requests to postpone closing

In these situations, extension costs are often the borrower’s responsibility.

Scenario 2: Lender-caused delay

Examples include:

- Internal processing delays

- Underwriting bottlenecks

- Operational issues within the lender

Some lenders may absorb certain extension costs when the delay is clearly attributable to their process.

Scenario 3: Third-party delay

Examples include:

- Appraisal scheduling

- Title work

- Government recording offices

- Builder delays

Responsibility varies by lender policy and transaction structure.

The important takeaway is that borrowers should understand extension policies before locking rather than after a delay occurs.

A simple framework: Compare expected cost, not just upfront cost

Many borrowers focus only on the cheapest lock period available.

A more useful approach is to compare total expected cost.

Consider the following illustrative example.

Option A: 30-day lock

Assume:

- Loan amount: $400,000

- 30-day lock cost: $0

- Probability of needing a 15-day extension: 30%

- Extension fee: 0.125 points

Extension cost:

- 0.125% × $400,000 = $500

Expected extension cost:

- $500 × 30% = $150

Expected total cost:

- $0 + $150 = $150

Option B: 45-day lock

Assume:

- Additional upfront lock cost: 0.05 points

Cost:

- 0.05% × $400,000 = $200

Expected total cost:

- $200

Option C: 60-day lock

Assume:

- Additional upfront lock cost: 0.10 points

Cost:

0.10% × $400,000 = $400

Expected total cost:

$400

In this example, the 30-day lock has the lowest expected cost.

However, if the probability of delay rises significantly, the comparison can change. The lesson is not that one option is always superior. The lesson is that lock duration should be evaluated using both cost and timeline risk.

Understanding extension fees

Extension pricing varies significantly by lender and market conditions.

Illustrative examples often include:

- Approximately 0.02% to 0.05% of the loan amount per day, or

- Approximately 0.125 to 0.25 discount points per extension period

These figures are examples only and may not reflect current lender pricing.

Actual costs can differ materially based on loan program, lock term, market conditions, and lender policy.

For that reason, borrowers should request specific extension pricing information before selecting a lock period.

A Better Conversation Than “What’s the Rate?”

Instead of asking only, “What is today’s rate?”, consider asking:

- How long is the lock period?

- What is the extension policy?

- How are extension fees calculated?

- What delays are most common for this transaction?

- Does a new construction property create additional timeline risk?

- What are the costs of 30-, 45-, and 60-day lock options?

These questions often provide more useful information than rate alone.

Final Thought

Example rate, fee, APR, and cost figures in this article are hypothetical and provided solely for educational purposes. They do not represent a commitment to lend, a loan approval, or current market pricing.

Disclaimer: Wonder Rates NMLS #1518655 Equal Housing Lender Rates and terms subject to change. This article is for educational purposes only and should not be considered financial, tax, or legal advice.

Leave a Reply