Loan officers are often mistaken for salespeople. It is an easy assumption to make when the first thing you hear is a rate quote. But that view misses most of what actually determines whether your loan gets approved or falls apart.

1. The Reality Behind the “Rate Quote”

You ask about rates, and your loan officer says something like: “Based on your profile, rates today are around 6.5%, but I cannot promise that until we lock it in writing, since things change daily.”

That can sound unclear. It is not.

Under federal rules, a loan officer cannot present a rate like a fixed price tag. Rates move daily with the market, and your final number depends on your full file, the appraisal, and when you lock. A good loan officer is not selling certainty. They are managing your expectations within the law.

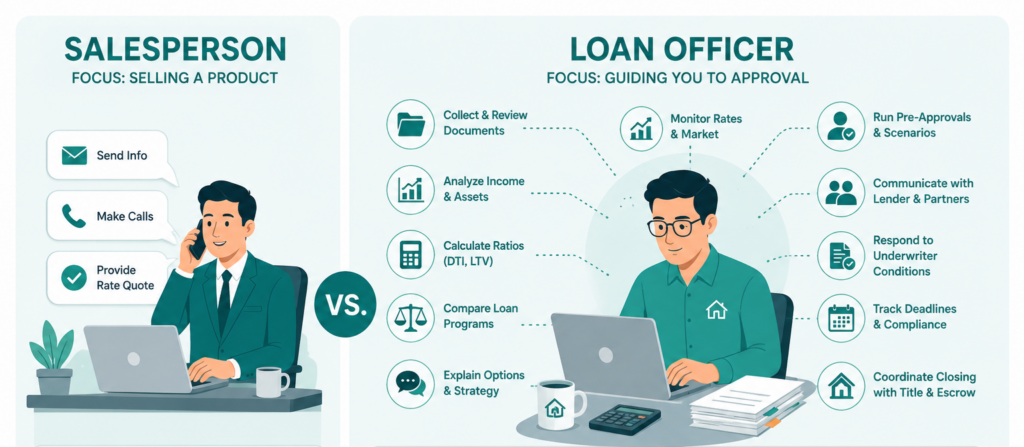

2. Who a Loan Officer Is and Is Not

A loan officer, officially called a Mortgage Loan Originator, is your bridge to the lender. They guide you from your first question all the way to closing day, translating your financial life into something a lender can evaluate.

But they are not the decision-makers. They are not the underwriter who approves or denies your loan, and they are not the appraiser who determines the home’s value. They are also not your real estate agent. Their role is narrower and more technical.

Their job is simple to describe, but hard to execute: build a file that gets approved.

3. Perception vs. Reality

From the outside, the job looks simple. A few emails, some calls, maybe a couple of rate quotes.

That is about 20% of it.

The other 80% happens where you never see it. Your loan officer spends hours fixing documentation issues, aligning your file with federal guidelines, and keeping the deal alive as conditions change. If the loan does not close, they usually do not get paid, which means weeks of work can end with nothing.

4. Income Reality: How They Actually Get Paid

Loan officers are typically paid in basis points, not by interest rate. One hundred basis points equals 1% of the loan amount.

For example, on a $400,000 loan, 100 BPS equals $4,000, while 50 BPS equals $2,000. Per industry survey, many retail loan officers earn roughly 90 to 105 BPS per funded loan, depending on experience and volume.

Here is the key detail that most buyers miss.

They are not paid more for giving you a higher rate.

Under Regulation Z, compensation cannot be tied to loan terms like the interest rate. It can be tied to the loan amount or overall production. This rule exists to prevent steering you into a worse deal for higher pay.

5. What Loan Officers Actually Do

The work usually breaks into two layers.

The first is what you see. This is the advisory side, where they compare loan options like Conventional, FHA, or VA based on your profile. They calculate your full monthly payment using PITI, including principal, interest, taxes, and insurance. They also move you from a rough estimate to a verified pre-approval, which strengthens your offer. If you’re buying a home for the first time, understanding where pre-approval fits into the home buying process can help you avoid delays later.

The second layer is where most of the real work happens. They analyze your income, especially if it is variable or self-employed, and track key ratios like DTI and LTV to keep your file within approval limits. They respond to underwriter conditions, which often require updated documents like bank statements, pay stubs, or tax returns.

A file can look strong at first glance and still fail if these details are not handled correctly.

6. Constraints and Pressure

Loan officers operate under strict regulatory timelines and rules. Under TRID guidelines, they must provide a Loan Estimate within three business days after your application. They cannot promise rates verbally, and they cannot guide you into a loan that benefits them more than you.

They also cannot receive compensation from both you and the lender on the same transaction. Every step is monitored to protect you as a consumer, which adds pressure behind the scenes that most borrowers never notice.

7. A Day in the Life

To understand the role, it helps to look at a typical day.

The morning often starts with checking rate sheets and pipeline updates. By mid-morning, they are calling clients and collecting missing documents. Late morning is spent running pre-approvals and calculating ratios, followed by coordinating with referral partners in the early afternoon.

The rest of the day is usually consumed by handling underwriter conditions and coordinating closing details with title and escrow.

Most of the day is not selling. It is problem-solving.

8. Key Insight

Approval is not luck. It is structure.

A loan gets approved because hundreds of small requirements are met at the same time, from income documentation to timing rules. When your process feels smooth, it usually means problems were solved before you ever saw them.

9. How to Verify Your Loan Officer

Every licensed loan officer in the United States has an NMLS ID, and you can verify it in less than a minute.

Go to https://nmlsconsumeraccess.org and search their name or NMLS number.

Check three things:

- The license status is active

- They are authorized to operate in your state

- There are no serious disciplinary actions

If anything looks unclear, ask questions before moving forward.

10. Conclusion

A loan officer is not just a salesperson. They are part analyst, part project manager, and part compliance guard.

The rate may get your attention, but the real value is invisible. It shows up in how your file is structured, how problems are solved, and how regulations are navigated to get you to closing.

That is what gets you the keys.

FAQs

Do loan officers set mortgage interest rates?

No. Mortgage rates are influenced by the market and your financial profile. A loan officer can quote an estimated rate based on current conditions, but the final rate is only confirmed when it is locked in writing with the lender.

Do loan officers earn more if you get a higher rate?

No. Under federal law, loan officer compensation cannot be tied to the interest rate or loan terms. They are typically paid based on the loan amount or overall production, not the rate you receive.

What does a loan officer actually do behind the scenes?

Most of their work involves reviewing documents, calculating ratios, responding to underwriter conditions, and making sure your file meets lending guidelines. This behind-the-scenes work is what keeps your loan on track to close.

How can you verify a loan officer is legitimate?

You can check their NMLS ID on the official NMLS Consumer Access website. This lets you confirm their license status, the states they are authorized in, and whether they have any disciplinary history.

Is a loan officer the same as a mortgage broker?

Not always. A loan officer typically works for a specific lender, while a mortgage broker may work with multiple lenders. However, both must follow the same federal rules regarding disclosure, compensation, and consumer protection.

Wonder Rates NMLS # 1518655

Equal Housing Lender

Disclaimer: This information is for educational purposes only and is not a commitment to lend.

Leave a Reply