What is a mortgage? Many first-time homebuyers ask this question when they begin exploring financing options.

Buying a home feels exciting until the financing part starts sounding confusing.

You hear terms like interest rate, escrow, PMI, or DTI, and suddenly you’re not sure what you’re agreeing to. Most first-time buyers reach this point.

The good news is that mortgages are easier to understand once you break them into smaller pieces. This guide explains how mortgages work, what makes up your monthly payment, and what lenders look for when reviewing your application.

If you’re planning to buy a home soon, it also helps to understand the overall home buying process before applying for a mortgage.

What Is a Mortgage and How Does It Work?

A mortgage is a loan used to purchase a home. You borrow money from a lender and agree to repay it over time, usually with interest.

The property serves as collateral for the loan. If payments stop for an extended period, the lender may have the legal right to take ownership of the property through foreclosure.

Most mortgages have repayment terms of 15 or 30 years.

A 15-year mortgage typically comes with higher monthly payments but lower total interest costs. A 30-year mortgage spreads payments over a longer period, reducing monthly payments while increasing the total interest paid over the life of the loan.

For example, borrowing $320,000 at a 6.5% interest rate on a 30-year mortgage produces a lower monthly payment than a 15-year mortgage, but the overall interest expense is significantly higher.

Once the loan is paid in full, the lender’s claim on the property is removed, and you own the home free and clear.

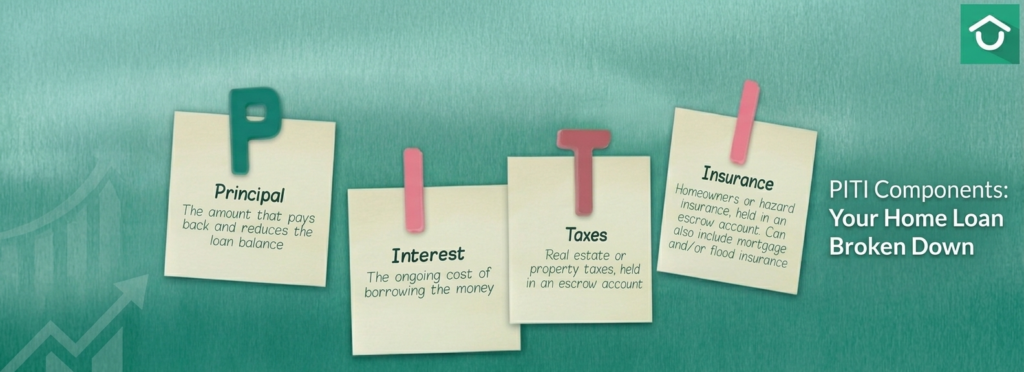

What Is Included in a Mortgage Payment? (PITI)

Your monthly mortgage payment is commonly referred to as PITI, which stands for:

Principal

The portion of your payment that reduces your loan balance.

Interest

The cost of borrowing money from the lender.

For example, a $320,000 mortgage at 6.5% generates a principal and interest payment of approximately $2,020 per month.

Taxes

Property taxes are often divided into monthly installments and collected with your mortgage payment.

Insurance

Homeowners insurance protects the property and is typically required by lenders.

Example Mortgage Payment

Home Price: $400,000

Down Payment: 20%

Loan Amount: $320,000

Estimated Monthly Payment

- Principal & Interest: $2,020

- Property Taxes: $367

- Homeowners Insurance: $125

Total Estimated Payment: $2,512 per month

Additional Costs in a Mortgage Payment

Depending on your loan type and financial situation, additional expenses may be included in your monthly payment.

PMI (Private Mortgage Insurance)

PMI applies to many conventional loans when the down payment is less than 20%.

It protects the lender, not the borrower.

In many cases, PMI can be removed once the loan-to-value ratio reaches 80%.

MIP (Mortgage Insurance Premium)

MIP applies to FHA loans.

Unlike PMI, MIP often remains for the life of the loan unless the borrower refinances into another mortgage program.

HOA Dues

Some properties located in planned communities or condominiums require monthly homeowners association fees.

Escrow Account

Many lenders collect money for taxes and insurance through an escrow account and pay those bills on your behalf when they become due.

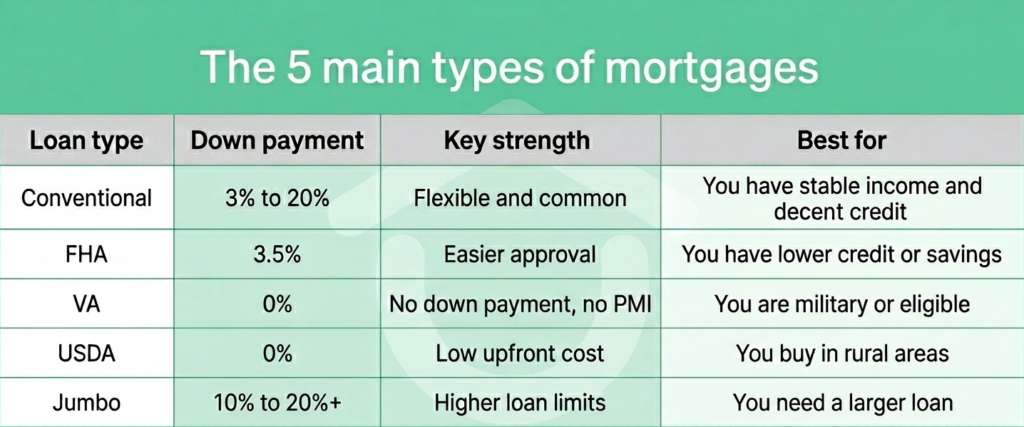

The 5 main types of mortgages

Each mortgage program serves a different purpose.

For example, FHA loans may be easier to qualify for, while VA loans provide significant benefits for eligible service members and veterans.

Fixed-Rate vs Adjustable-Rate Mortgages

A fixed-rate mortgage keeps the same interest rate throughout the loan term.

This means your principal and interest payment remains predictable.

An adjustable-rate mortgage (ARM) begins with a fixed rate for a specific period and then adjusts periodically based on market conditions.

For example, a 5/1 ARM maintains the same rate for five years before adjusting annually.

Fixed-rate mortgages offer stability, while ARMs may provide lower initial rates in exchange for future uncertainty.

Why Early Mortgage Payments Go Mostly to Interest

Many first-time buyers are surprised to learn that early mortgage payments contain more interest than principal.

This happens because interest is calculated based on the remaining loan balance.

At the beginning of the loan, the balance is at its highest point, so more of each payment goes toward interest.

As the balance gradually decreases, a larger portion of your payment goes toward reducing principal.

This repayment structure is known as amortization.

How to Qualify for a Mortgage

Understanding how mortgages work is only the first step.

Lenders also evaluate whether you are likely to repay the loan successfully.

Credit Score

Higher credit scores generally improve approval odds and may help borrowers qualify for lower interest rates.

Debt-to-Income Ratio (DTI)

DTI compares your monthly debt obligations to your monthly income.

Lower ratios are typically viewed more favorably by lenders.

Down Payment

A larger down payment reduces risk and lowers the amount borrowed.

Loan-to-Value Ratio (LTV)

LTV measures the loan amount compared to the home’s value.

Lower LTV ratios generally indicate lower risk.

Common Documents Required

- Proof of income

- Tax returns

- Bank statements

- Government-issued identification

Mortgage Pre-Qualification vs Pre-Approval

Pre-qualification provides a basic estimate based on information supplied by the borrower.

Pre-approval involves documentation review and a credit check.

Because pre-approval verifies financial information, it generally carries more weight with sellers.

In competitive housing markets, a pre-approval letter can strengthen your offer and improve your chances of securing a home.

Mortgage FAQs

What is a mortgage in simple terms?

A mortgage is a loan used to purchase a home and repay it over time through monthly payments.

Is a mortgage the same as a home loan?

In most cases, the terms “mortgage” and “home loan” are used interchangeably.

How much mortgage can I afford?

The amount depends on your income, debts, credit score, down payment, and other financial factors.

What credit score do I need for a mortgage?

Requirements vary by lender and loan program, but many conventional mortgages prefer scores of 620 or higher. The Consumer Financial Protection Bureau provides additional resources to help first-time buyers understand mortgage requirements and prepare for the application process.

Bottom Line

A mortgage allows you to buy a home now and pay for it over time through structured monthly payments.

Once you understand how mortgages work, comparing loan options, monthly costs, and qualification requirements becomes much easier.

For many first-time buyers, the best next step is reviewing their credit profile and obtaining a mortgage pre-approval before beginning their home search. Understanding the role of a loan officer can also help you navigate the mortgage process more confidently.

Ready to Take the First Step?

Talk to a licensed loan officer and review your real numbers. Even a short conversation can help you understand what you can realistically afford and which mortgage options may fit your goals.

Disclaimer

Wonder Rates NMLS #1518655. Equal Housing Lender. This content is for informational purposes only and does not constitute financial, legal, or tax advice. Mortgage products, interest rates, and underwriting guidelines vary by lender and are subject to change without notice. This is not a commitment to lend. All loan applications are subject to credit and property approval.