Most buyers know they need a mortgage, but few understand what really happens between getting pre-approved and receiving the keys. Follow Wonder Rates to explore the 10 essential steps every homebuyer should know before closing.

NMLS #1518655

What Is the Homebuying Process? The 10 Steps to Buying a Home in the US

The homebuying process is the series of steps that takes you from deciding to purchase a home to receiving the keys on closing day. While every transaction is unique, most buyers follow the same general path. Along the way, you’ll work with real estate agents, mortgage professionals, appraisers, inspectors, and title companies. Knowing what happens at each stage can help you stay organized and reduce stress throughout the journey.

How Long Does It Take to Buying a Home in the US?

In the US, the homebuying process usually takes about 30–45 days from the time your offer is accepted until closing and you get the keys.

But in real life, it can take longer depending on how fast you prepare and find a home. The process is usually split into 2 main phases:

1. Before making an offer (flexible time)

This is the preparation stage:

- You set your budget to see what you can really afford (not just the home price, but also taxes and insurance)

- You get pre-approved by a lender to show you are qualified to buy

- You start house hunting, visit homes, and pick the one you like

2. After your offer is accepted (30–45 days)

Once the seller accepts your offer, the home goes “under contract” and things move faster:

- You put down earnest money into an escrow account

- You do a home inspection to check the condition of the house

- The lender does an appraisal to check the home’s value

- Then comes underwriting, where the bank reviews your full loan file

- Finally, closing: you sign the final papers, the loan is funded, and you get the keys

What can slow things down?

A few common delays include:

- The home appraises lower than the purchase price

- The bank asks for more documents

- Paperwork processing takes longer than expected

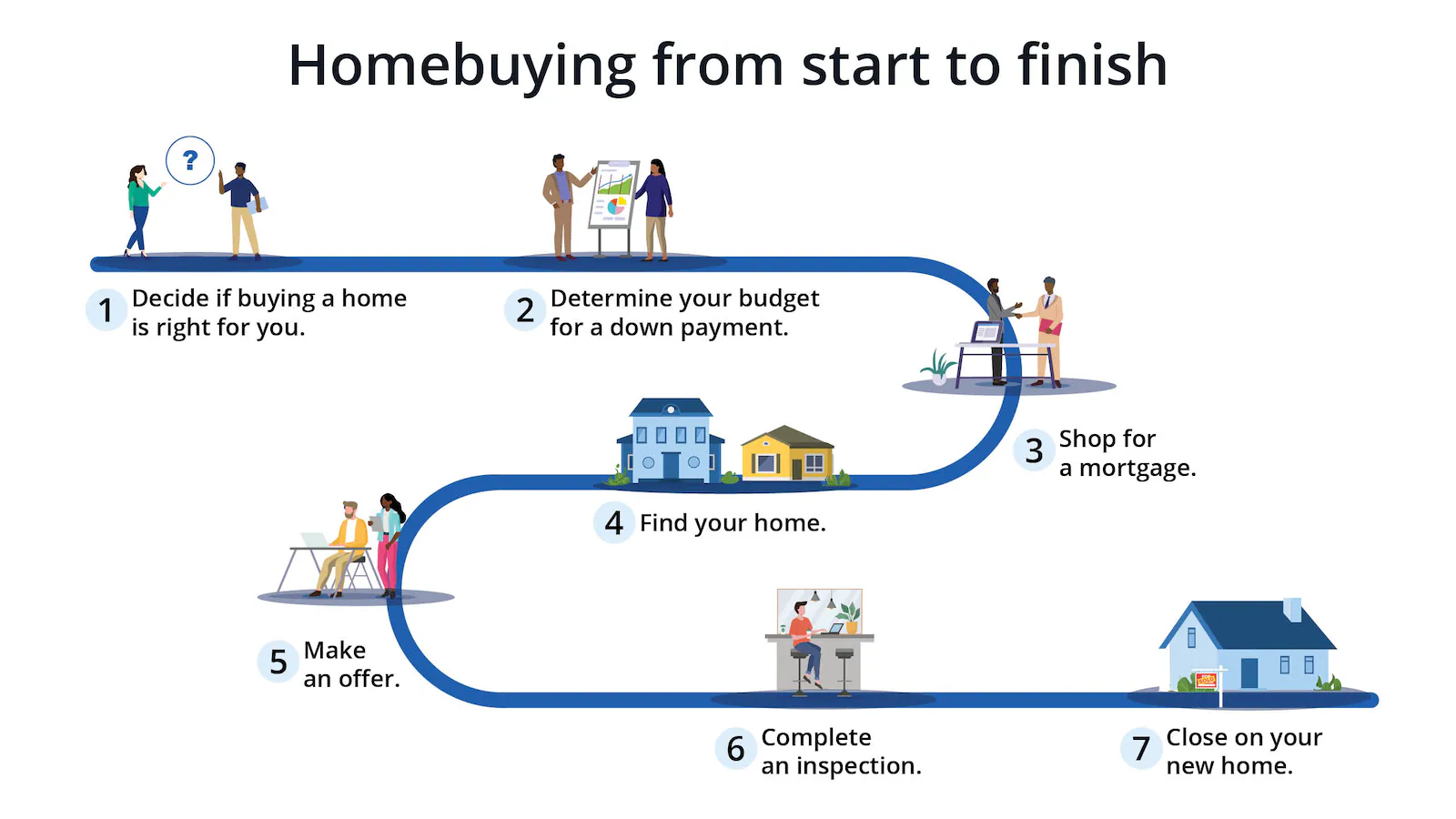

The 10 Steps to Buying a Home in the US

Buying a home may seem complicated, but most transactions follow a predictable process. From determining your budget to signing the final paperwork, each step plays an important role in helping you become a homeowner. Here’s a quick overview of the 10 key steps you’ll typically go through when buying a home in the United States.

| Step | What Happens |

|---|---|

| 1. Determine Your Budget | Review your income, savings, debts, and monthly expenses to understand how much home you can comfortably afford. |

| 2. Get Pre-Approved for a Mortgage | A lender reviews your financial information and provides a pre-approval letter showing how much you may be eligible to borrow. |

| 3. Choose a Real Estate Agent | An experienced agent helps you find homes, negotiate offers, and navigate the buying process. |

| 4. Start House Hunting | Search for properties that fit your budget, preferred location, and lifestyle needs. |

| 5. Submit an Offer | Work with your agent to prepare and submit a purchase offer to the seller. |

| 6. Open Escrow and Deposit Earnest Money | Once your offer is accepted, you’ll deposit earnest money and open escrow to begin the transaction. |

| 7. Complete the Home Inspection | A licensed inspector evaluates the property’s condition and identifies potential concerns. |

| 8. Complete the Appraisal | The lender orders an appraisal to confirm the home’s market value. |

| 9. Go Through Underwriting | The lender reviews your finances, documents, and property information before issuing final approval. |

| 10. Receive Clear to Close and Attend Closing | Sign final documents, complete funding, and officially become a homeowner. |

Common Mistakes Homebuyers Should Avoid

Even when people understand the overall homebuying process, a few common mistakes can create confusion, delays, or unexpected costs. Here are some of the most important ones to watch for:

Forgetting Property Taxes and Insurance

- Many buyers calculate affordability using only principal and interest.

- Always use PITI (Principal, Interest, Taxes, and Insurance) to estimate your true monthly housing cost.

Confusing Earnest Money with the Down Payment

- Earnest money is a good-faith deposit submitted after an offer is accepted.

- The down payment is the larger amount applied toward the home’s purchase price at closing.

Mixing Up PMI and MIP

- PMI applies to conventional loans with less than 20% down.

- MIP applies to FHA loans.

- These mortgage insurance programs are not interchangeable.

Getting Inspection and Appraisal Out of Order

- The buyer typically orders the home inspection first to identify property issues.

- The lender then orders the appraisal to determine the home’s market value.

Overlooking the Title Search

- A title search helps uncover ownership disputes, liens, or legal claims against the property.

- Skipping this step can lead to serious legal and financial problems.

Misunderstanding Closing Documents

- The buyer signs the Note and Mortgage documents.

- The seller signs the Deed, which officially transfers ownership of the property.

How to Take Action

Start by reviewing your finances and understanding how much home you can realistically afford. Before you begin house hunting, obtain a mortgage pre-approval so you know your budget and can make stronger offers when you find the right property.

It’s also important to work with trusted professionals throughout the process, including a knowledgeable real estate agent and a licensed loan officer. If you’re looking for guidance on mortgage options, loan requirements, and the homebuying process, consider partnering with a reputable mortgage company such as Wonder Rates. Having the right team by your side can help you navigate each step with confidence, avoid costly mistakes, and stay on track toward closing day.

Keep your financial documents organized, respond quickly to lender requests, and don’t hesitate to ask questions along the way. Taking these steps early can make your homebuying journey smoother, faster, and less stressful.

Bottom Line

Buying a home involves multiple steps, but understanding the process can make it much less intimidating. By preparing early and working with the right professionals, you can move from house hunting to homeownership with confidence.

Want help choosing the right loan? Talk to one of our licensed loan officers at ……

Disclaimer: Wonder Rates NMLS #1518655 Equal Housing Lender. Information is provided for educational purposes only and is not a commitment to lend. Loan approval, rates, and terms are subject to lender review and applicable underwriting requirements.

Leave a Reply